We are currently witnessing a masterclass in misdirection. Following the recent ₹3 per liter hike in petrol and diesel prices, the Prime Minister took to the stage to make a highly publicized seven-point appeal to the nation. We are being asked to work from home, use public transport, delay foreign travel, and, most notably, halt the purchase of gold for the next year.

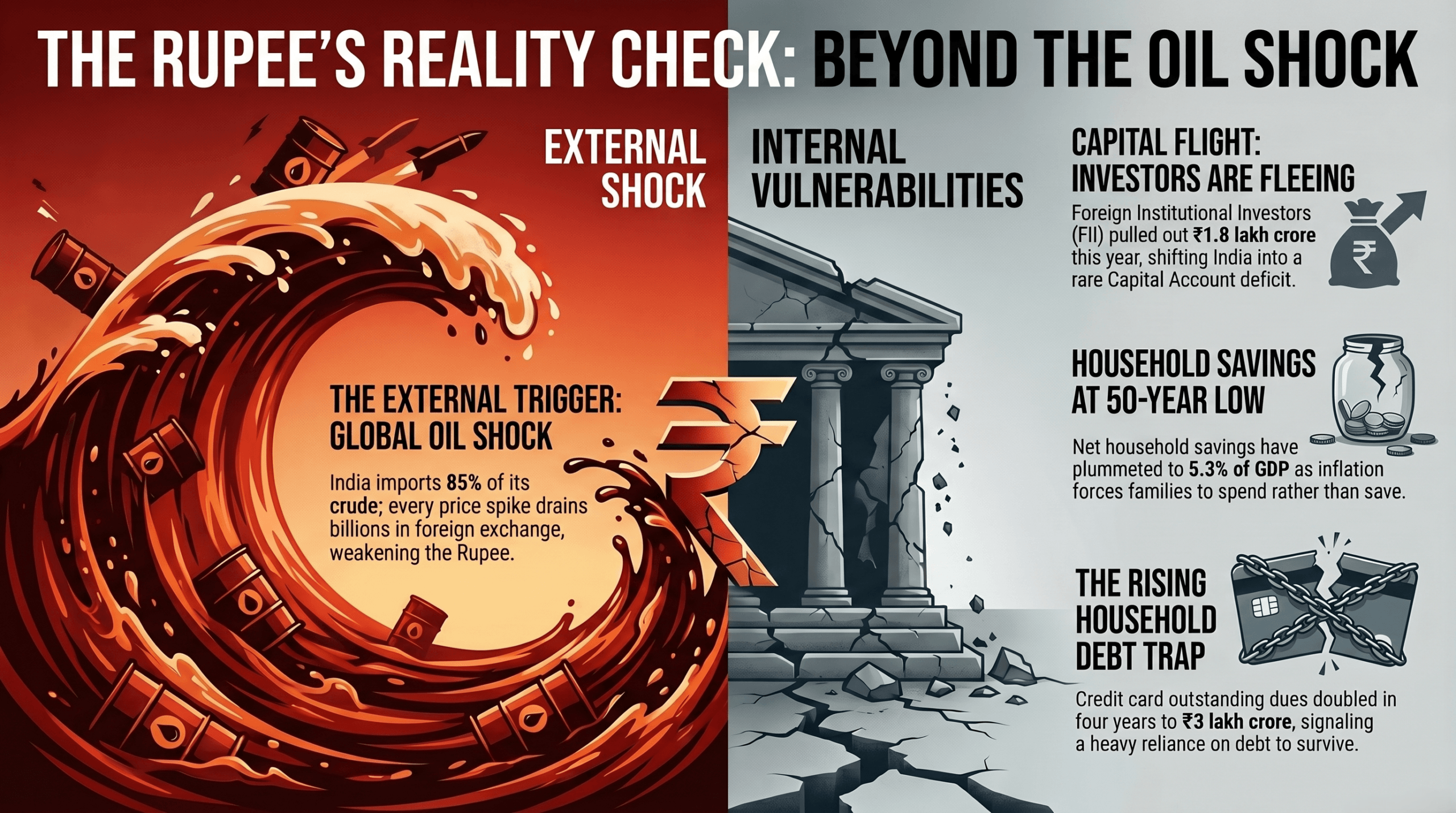

The narrative being spun is that this austerity is a necessary patriotic duty to shield our economy from the global fallout of the US-Iran conflict and the subsequent blockade of the Strait of Hormuz. While it is undeniably true that the geopolitical crisis has choked global supply chains and spiked energy costs, blaming the current state of the Indian economy entirely on an external oil shock is a dangerous half-truth. The uncomfortable reality is that our economic foundations were cracking long before the first shots were fired in the Middle East.

The Illusion of the Consumption-Led Boom

For years, we have patted ourselves on the back for being the “fastest-growing major economy,” fueled largely by a domestic consumption model rather than an export-driven one like China, South Korea, or Taiwan. But this model has a fatal flaw. When an economy grows primarily through consumption without a matching manufacturing and export base, it inevitably leads to a massive import bill.

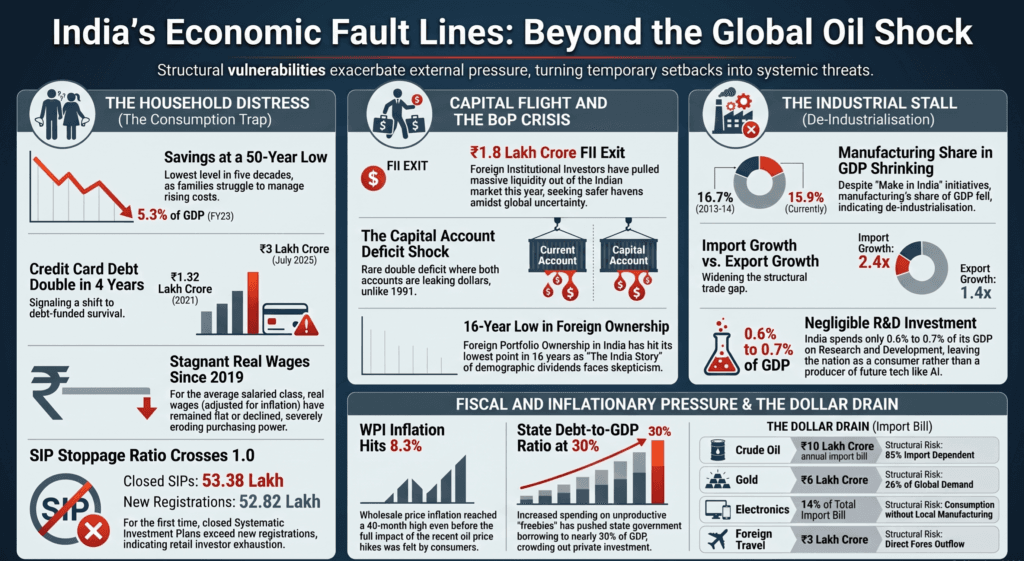

We import 85% of our oil and 26% of the world’s gold, resulting in a permanent current account deficit. Historically, we patched this leak through a surplus in our capital account—relying on Foreign Direct Investment (FDI), Foreign Portfolio Investment (FPI), and remittances. But the music has suddenly stopped. For the first time in recent memory, India is facing a capital account deficit in 2025. Foreign institutional investors have pulled out a staggering ₹1.8 lakh crore this year alone, drastically shrinking the RBI’s foreign currency reserves. The world is losing faith in the “India Story,” and our weakening rupee is the direct consequence of dollars fleeing the country.

Structural Rot and the Middle-Class Squeeze

If we look beyond the geopolitical smokescreen, the domestic indicators are chilling. Wholesale Price Index (WPI) inflation surged to 8.3% in April—a 40-month high—indicating that inflation was already ravaging the economy before the Iran crisis escalated.

The root of this domestic inflation is political, not global. State governments, desperate for electoral victories, have turned to distributing massive unconditional freebies, driving up state deficits and forcing the RBI to inject artificial liquidity into the market. As economist Prof. Prasanna Tantri points out, this “too much money chasing too few goods” scenario laid the perfect groundwork for an inflation explosion long before crude oil prices spiked.

Meanwhile, the everyday Indian is suffocating. Real wages for the salaried class have effectively stagnated or declined since 2019. Consequently, net household savings have plummeted to a 50-year low of just 5.3% of GDP. With no savings to fall back on, the middle class is surviving on debt; outstanding credit card dues have more than doubled from ₹1.32 lakh crore in 2021 to nearly ₹3 lakh crore. Furthermore, despite the hype around “Make in India,” manufacturing’s share of our GDP has actually shrunk from 16.7% a decade ago to a mere 15.9% today, a clear sign of de-industrialization.

Flawed Solutions: Why “Moral Suasion” Isn’t Enough

The government’s solution to this deep-rooted structural crisis? Asking citizens to stop buying gold.

While moral suasion might sound good in a political rally, it is a remarkably blunt and ineffective economic tool. Gold is not merely a hobby for Indians; it is a vital hedge against the very inflation and currency devaluation the government has failed to control.

If the government genuinely wants to fix the crisis, it needs to abandon PR-driven appeals and implement hard economic reforms. Former Finance Commission Chairman Arvind Panagariya suggests letting the rupee naturally depreciate, which would automatically make all imports more expensive and exports more competitive, organically balancing the current account deficit without singling out specific industries.

Additionally, instead of squeezing the consumer, the government must look inward. The Centre collects nearly ₹3.8 lakh crore in excise duties, primarily from petrol and diesel. Instead of passing the entire burden of global oil prices onto an already debt-ridden public, the government should slash these excise duties. How do we fund this? By trimming the fat from our bloated, politically-driven ₹12 lakh crore capital expenditure budget. We must stop funding economically unviable projects—like subsidizing airfares at empty district airports or running premium trains on taxpayer money—and redirect those funds to stabilize the economy.

My Final Take

It is time to stop hiding behind the excuse of the Strait of Hormuz. The global oil shock is merely the catalyst that exposed the fragile, debt-fueled, and structurally flawed reality of India’s current economic model. We cannot PR our way out of a capital flight, nor can we cure a 50-year low in household savings by simply telling people to work from home.

Until our leadership moves beyond divisive politics and addresses the severe lack of manufacturing jobs, the stagnation of wages, and the unsustainable culture of political freebies, this crisis will only deepen. The time for tall claims and makeup-laden statistics is over; the time for accountability and structural reform is right now.